Pasture, Range and Forage Insurance for Good Range Management

By John Walker, Texas A&M AgriLife Research

Rain is arguably the most important factor for successful ranching. While it is true that little can be done to affect the amount of rain that falls, there is much that can be done to ensure the rain stays where it falls.

The key to keeping as much of the rain where it falls is to have adequate grass cover. Research at the Sonora AgriLife Research Station showed that infiltration doubled for each percentage unit increase in vegetative soil cover.

This may seem like an odd introduction to an article on Pasture, Range and Forage Insurance (PRFI), also known as rainfall insurance, but as a range scientist I believe it is important to put management decisions in the context of creating healthy sustainable rangelands. Used appropriately PRFI can provide the economic flexibility to improve range condition and increase infiltration of rainfall.

A brief overview of precipitation patterns is in order before considering rainfall insurance. Most will agree there is no such thing as an average year, but there is still a need for a standard to compare the current situation with the past.

Median annual rainfall is the best estimate of normal in the semi-arid ranch country. Take annual rainfall amounts for an odd number of years and arrange them from highest to lowest. The number in the middle is the median.

In San Angelo the long-term median rainfall is 20 percent less than the average rainfall. The prudent ranch manager will stock his or her pastures and manage his or her ranch for the median rainfall and insure for the average rainfall.

The USDA Risk Management Agency (RMA) made Pasture, Range and Forage Insurance based on the estimated rainfall in a 12-by-12-mile grid available as a pilot program in selected states in the 2007 crop year.

The program insurance is subsidized from 51 to 59 percent of the premium cost, but when rainfall is below the selected coverage level the insured receives 100 percent of the indemnity.

This insurance is considered rather simple because there are no reporting or record-keeping requirements for PRFI. After an individual signs up, his or her paperwork is essentially done.

Claims are calculated based on a chosen coverage level and are paid automatically. However, there are many decisions on the front end that can make the program seem complicated.

Four decisions

There are 4 basic decisions to consider, and there are levels within each of the decisions.

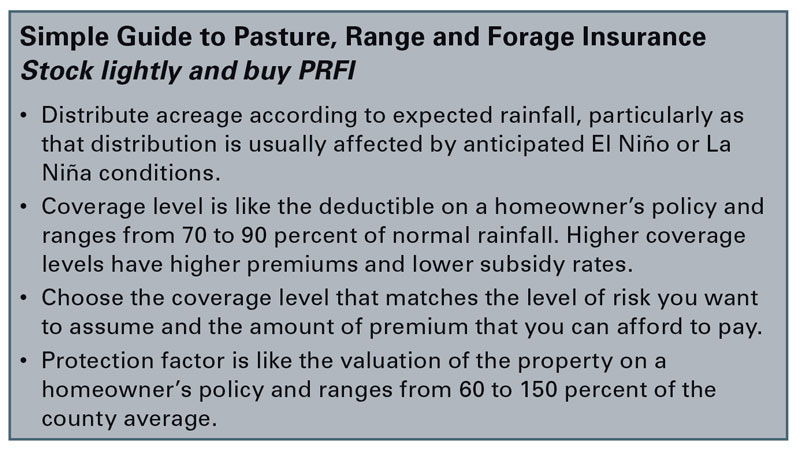

- Acreage

Individuals can insure all or part of their property, but most commonly the entire property is insured. This is the easiest decision.

- Coverage level

This ranges from 70 to 90 percent of average rainfall. The final grid index must be below the chosen coverage level to trigger a payment. This also affects the amount of subsidy that is provided. RMA pays 59 percent of the premium for the 70 and 75 percent coverage level and 51 percent of the premium for the 90 percent coverage.

- Protection factor

This ranges from 60 to 150 percent and allows individualization based on how productive a property is compared to average property in that county.

- Index intervals

There are 11 2-month intervals. Two to 6 intervals must be insured with a minimum of 10 percent of the enrolled acreage insured for any chosen interval. This is the most important and the most complicated of the decisions that must be made when taking out PRFI.

Complex but familiar

I decided to investigate the consequences of the many decisions one must make in deciding on rainfall insurance. I based my research on historic index values for the area where the Texas A&M AgriLife Research and Extension Center is in northwest Tom Green County.

To do this I calculated the net returns for all possible combinations of 5 coverage levels, 10 protection factors and 56 combinations of the 11 intervals for a 64-year period beginning in 1948, the year for which historic index values are available from RMA. This resulted in a total of 214,400 outcomes.

Before describing the results of this study I would like to describe some of the complexities of PFR insurance. Premiums and indemnities are based in part on the county base value per acre of pasture. For Tom Green County that amount is $8.25 per acre.

If the lease rate for an animal unit month of grazing is $13.50, as estimated by Extension budgets, this would be equivalent to an annual stocking rate of 20 acres per animal unit.

If you insure for the actual long-term sustainable stocking rate and that stocking rate is higher or lower than the county average, then the protection factor can be adjusted to reflect this.

For instance, if the long-term carrying capacity for your ranch is 30 acres per animal unit, then a protection factor of 66 percent would be appropriate if you insure for the actual carrying capacity of the ranch. Thus the protection factor is similar to the value placed on your home for a homeowner’s insurance policy.

The coverage level is like the deductible on an insurance policy. The more risk you are willing to assume the lower the premium. There are 5 coverage levels between 90 and 70 percent, in increments of 5 percent. The level of subsidy declines as the coverage level increases.

At 90 percent coverage the insured will receive an indemnity if the rainfall is less than 90 percent of the long-term average and RMA pays 51 percent of the premium.

At the 75 and 70 percent coverage levels, an indemnity is paid if the rainfall is less than 75 or 70 percent, respectively, and RMA pays 59 percent of the premium. The premium is also higher for the 75 percent coverage level compared to the 70 percent coverage level because the actuarial probability of falling below 75 percent is greater than falling below 70 percent of long-term average precipitation.

Premiums are highest for the fall and winter months — when rainfall is less variable — than for the spring months, which have a greater amount of variability because of convectional thunderstorms.

Fall and winter months are also more likely to be affected by El Niño and La Niña events.

Premium cost for our area of Tom Green County is $25 to $35 per $100 of coverage for the November-to-February period compared to $10 to $25 for the May-to-June period. Compared to homeowner’s insurance, which is about $1 per $100 of coverage in this area, PRFI is very expensive. This is because we expect drought every few years. In contrast, most people hope they never have to make a claim on their homeowner’s policy.

Can’t outguess the weather

If you decide to take out PRFI you should commit to taking it out every year and not try to outguess the weather.

Again, compare this to homeowner’s insurance. Most people with homeowner’s insurance keep coverage every year even though they may never make a claim. Consider how much more important it is to keep PRFI in place for drought, which you do expect to happen. People who dropped their PRFI after paying high premiums in 2010 sorely regretted it in 2011, Texas’ driest year on record.

Important discoveries

Two important discoveries were made based on the study involving the 214,400 scenarios for rainfall insurance.

First, averaged across 64 years there was no difference in net return for taking out PRFI for the different combinations of the 2-month intervals investigated.

However, averaged across these same 64 years, net returns varied 4-fold depending upon the coverage level and protection factor selected.

On average, higher coverage levels and higher protection factors have a higher net return.

This happens even though the subsidy rate is lower at the higher coverage level. The higher return is a result of leveraging more premium subsidy dollars at the higher coverage levels and protection factors. But this also exposes the insured to a much higher potential premium if rainfall exceeds the selected coverage level.

Wise decisions with weather knowledge

Precipitation in West Texas is affected by El Niño and La Niña events, which are referred to as the Oceanic Niño Index (ONI). These events have the greatest effect in the winter months when El Niño tends to have cooler, wetter weather and La Niña coincides with warmer drier winters.

Can knowledge of these cycles assist in making wise PRFI decisions?

Beginning in 1950, years were classified as an El Niño, La Niña, or neutral year and analyzed for net returns averaged across all years and all 11 intervals.

The results showed that net return for 34 neutral years and 14 El Niño years was about $0.45 per acre compared to 14 La Niña years that had a net return of $1.15 per acre — or more than 2 times as much.

Clearly such information can be useful, but this analysis was made after the fact. The closing date for PRFI is Nov. 15, which means that decisions must be made based on the mid-October predictions of the ONI for the coming year.

Historical ONI predictions are available at the Columbia University International Research Institute for Climate and Society for the 9-year period from 2003 to 2011.

The predictions were 66 percent accurate. However, predictions of the 2 La Niña years (2008 and 2011) were 100 percent accurate.

Averaged across all intervals, net returns for the 7 neutral or El Niño years were only slightly above 0 but for the 2 La Niña years the net returns were $1.62 per acre.

Decisions about how to participate in PRFI can be boiled down to 2 questions. First, how much risk can the ranch handle? Second, what are the expectations for rainfall distribution in the coming crop year?

Over the long-term, maximizing the coverage level and the protection factor will maximize net return. It will also maximize the loss in any interval that receives rainfall in excess of the selected coverage level. But, the insured has to be able to pay the total premium in any given year without it having a catastrophic effect on the business.

Calculate the maximum potential premium for the chosen coverage and protection and consider the impact of this cost on the business. PRFI will always provide a positive net return over the long term, but bankruptcy does not allow you to participate in the long term.

The best strategy for distributing coverage across intervals is to base decisions on the most current long-term weather forecasts available prior to taking out the insurance and on the historic indexes for previous similar situations relative to the projected condition of the ONI.

The National Weather Service makes long-term predictions. Go to weather.gov and search for Climate Prediction Center. Once you have reached National Weather Service Climate Prediction Center page, navigate to Outlooks (Forecasts) in the left column and click on Products.

There are also other free and paid forecasting services. However, the farther out a prediction, the less reliable the forecast. Beyond 6 months in the future, the probability of above- or below-normal precipitation is usually equal.

Insure the intervals with the highest probability of having below-average precipitation based on reputable forecast and the historic effect of ONI on the index value for the grid in which you are interested.

Insuring all intervals evenly will slightly decrease the risk of paying a premium in a single year but greatly decreases the long-term net return.

PRFI helps to protect livestock producers from lost income as a result of drought that reduces carrying capacity and livestock sales. It does not protect the producer from the vagaries of the market which often work against producers who have been forced to liquidate livestock because of drought in a down market.

However, PRFI when used to offset lost income as a result of light-to-conservative stocking rates can reduce exposure, because reduced stocking rates decrease the need to sell animals in a drought.

Using this strategy, except during exceptional drought, producers should be able to maintain their herds with little additional feed cost and receive an insurance payment that would compensate for reduced income as a result of having a smaller herd.

In above-average rainfall years they can use the additional forage for range improvement. Or they can purchase stockers or lease grazing to other producers and use the income to pay the premium.

PRFI is a good investment that can be made better by wise decisions regarding the coverage level, protection factor and distribution of coverage across intervals.

It can help reduce management decisions and exposure to down markets often associated with a drought.

Finally, and perhaps most importantly, it can help justify a range management program that will maximize the benefit of every drop of rain that falls on a ranch.

“Pasture, Range and Forage Insurance” is excerpted from the October 2013 issue of The Cattleman magazine.